")

The Philippine office market outlook for the second quarter of 2026 has become more uncertain amid ongoing geopolitical tensions, which have already dampened demand in the first quarter, and a stubborn elevated vacancy level.

“The escalating energy crisis and broader geopolitical tensions introduce downside risks that could slow deal conversions and weigh on occupier confidence,” said Mikko Barranda, Director of Commercial Leasing at Leechiu Property Consultants, during its 1Q 2026 Philippine Market Report.

The market opened the year with 234,000 square meters of gross demand in the first quarter, marking a 22 percent quarter-on-quarter decline, although this aligns with typical seasonal patterns. Net demand, however, reached 133,000 sqm, up 77 percent year-on-year, driven by a sharp drop in vacated spaces.

“Although office net demand is positive for 1Q 2026, rising geopolitical uncertainty and the ongoing energy crisis warrant close monitoring in the quarters ahead,” Barranda added.

Elevated vacancy levels

According to the report, the pipeline for office space supply in Metro Manila is projected to reach 807,000 sqm through 2028, with Quezon City accounting for the largest share at 240,000 sqm.

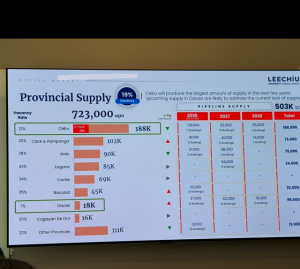

Total office stock stands at approximately 2.7 million sqm in Metro Manila and 723,000 sqm in provincial areas.

Vacancy levels remain elevated, particularly in key business districts across Metro Manila, prompting landlords to offer more flexible rental terms.

Data from Leechiu Property Consultants showed that vacancy rates stood at 18 percent in Metro Manila and 19 percent in Cebu.

The Bay Area and Mandaluyong posted the highest vacancy rates at 29 percent each, followed by Taguig City at 22 percent and Alabang at 21 percent.

Meanwhile, Bonifacio Global City recorded the lowest vacancy rate at 8 percent, followed by the Makati Central Business District at 9 percent. Makati City posted a 14 percent vacancy rate, while Ortigas City recorded 16 percent.

“BGC and Makati CBD, with single-digit vacancies and limited new supply, remain positioned for faster rental recovery. The sector’s trajectory in the coming quarters will depend on the duration of external disruptions and the pace at which pipeline requirements convert to committed deals,” said Barranda.

Provincial supply

Vacancy rates in provincial markets were slightly higher at 19 percent.

Among major provincial business districts, Laguna posted the highest vacancy rate at 43 percent, followed by Bacolod at 35 percent and Cavite at 34 percent.

Davao recorded the lowest vacancy rate at 7 percent, followed by Cebu at 12 percent. Cagayan de Oro, Clark, and Pampanga each posted vacancy rates of 20 percent.

“At this point, the market remains on track, but the path forward is becoming less straightforward. Tenants are becoming more discerning and intentional in their real estate decisions, which must be matched by greater flexibility from the market. While the demand pipeline remains healthy, the key risk lies in conversion, as to whether these requirements can translate into actual transactions amid current uncertainties. This is something we will need to monitor closely in the coming months,” Barranda added.