The rapid rise in demand for critical energy transition minerals (CETMs), driven by the expansion of clean energy technologies, electrification, and digitalization, is prompting countries to adopt critical minerals trade policies that are intensifying competition and, in some cases, restricting access to these resources, according to a new insight from the United Nations Conference on Trade and Development (UNCTAD).

UNCTAD’s latest global trade update, “The shifting dynamics of critical minerals trade,” said trade policies are becoming more significant as clean technologies account for an increasing share of mineral demand. Between 2024 and 2040, the share of nickel demand from clean technologies is projected to rise from 17 percent to 42 percent, while demand for magnet rare earth elements is expected to increase from 21 percent to 31 percent.

However, the report warned that the trade policy environment surrounding CETMs is undergoing a significant transformation that is leading to fragmentation rather than cooperation.

“Both exporting and importing countries are increasingly deploying trade policy as a strategic instrument to achieve their broader economic, industrial, and geopolitical objectives,” it noted.

The growing use of international CETM partnership agreements between producer and consumer countries is also reshaping market dynamics, often prioritizing supply security, resilience, and strategic alignment over cost efficiency.

This trend is intensifying competition for access to critical minerals. In this context, UNCTAD said trade policy is playing a larger role in determining where, how, at what cost, and for whose benefit CETMs are produced, processed, and traded across the global economy.

For developing countries endowed with significant CETM resources, the evolving landscape presents both opportunities and risks.

On one hand, strong global demand could generate higher export revenues, attract foreign direct investment, and create opportunities to develop downstream processing and manufacturing industries that support structural transformation. On the other hand, there is a risk of reinforcing traditional extractive models in which countries continue exporting raw materials with limited domestic value addition. While well-intentioned, partnership agreements may also contribute to an increasingly fragmented regulatory landscape.

Supply chain concentration

Although each CETM market has distinct characteristics, the UNCTAD update said that supply is generally marked by high geographic concentration across the value chain—from reserves and mining to processing and refining—with a small number of countries dominating global output.

Reserves of key minerals such as lithium, cobalt, rare earth elements, and nickel are unevenly distributed, with a handful of countries controlling a dominant share. This concentration extends to mining, where a limited number of countries and firms account for most global extraction.

The UNCTAD update cited data from the U.S. Geological Survey’s Mineral Commodity Summaries 2026, noting that in 2025 the Democratic Republic of the Congo accounted for 50 percent of global cobalt reserves and 74 percent of cobalt mine production. Indonesia produced 67 percent of global nickel mine output, while China accounted for 69 percent of rare earth production and 78 percent of natural graphite mine production. Australia, Chile, and China together generated 72 percent of global lithium mine production.

Mining is capital-intensive and characterized by long development timelines, limiting short-term supply responsiveness and leaving concentrated supply chains vulnerable to geopolitical risks, governance challenges, and environmental and social pressures.

Refining and other downstream activities are even more concentrated, creating critical bottlenecks in CETM supply chains. China dominates refining for rare earths, lithium, and cobalt, while Indonesia leads nickel refining, accounting for 43 percent of global capacity.

Refining requires substantial long-term investment, advanced technologies, specialized infrastructure, significant energy inputs, and economies of scale, creating high barriers to entry for new players. As a result, value-added activities remain highly centralized, shaping trade patterns and raising concerns about supply chain resilience and the distribution of economic benefits.

Although efforts to diversify processing capacity, expand recycling, and strengthen domestic value chains are increasing across countries and regions, these transitions are long-term endeavors that require significant investment and coordinated policy support.

The main manufacturing sectors that depend on CETMs are concentrated in a few rapidly growing, technology- and energy-intensive industries. High-performance permanent magnets containing rare earth elements illustrate this dynamic. They are indispensable components in advanced manufacturing, powering everything from electric vehicle traction motors, wind turbine generators, aerospace systems, and defense actuators and consumer electronics systems.

Because these sectors involve high value addition, technological complexity, and strong manufacturing linkages, countries with processing and industrial capacity are able to capture a substantial share of CETM-related economic benefits.

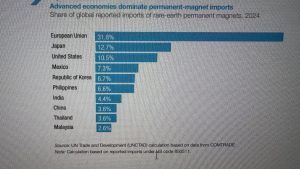

Imports of rare-earth permanent magnets are heavily concentrated in industrialized economies. In 2024, the European Union, Japan, and the United States accounted for 55 percent of global imports. These economies use imported magnets to manufacture high-value finished products, underscoring that most CETM value is captured not at the extraction stage but in processing and advanced manufacturing.

Notably, the Philippines ranked sixth among the top 10 importers of rare-earth permanent magnets, accounting for a 6.6 percent share of global imports. Other countries in the top 10 include Mexico (4th), South Korea (5th), India (7th), China (8th), Thailand (9th), and Malaysia (10th).

Trade policies

Since 2020, critical-mineral-rich countries have increasingly adopted export-restrictive measures, primarily in the form of licensing requirements, export taxes, and export bans. These measures are intended to strengthen oversight of exports and safeguard national security.

In recent years, however, governments have increasingly turned to more stringent tools, including export bans and other quantitative restrictions.

The UNCTAD update showed that the Democratic Republic of the Congo has introduced 18 export measures, the highest number among surveyed countries, followed by China with 16 and Indonesia with 12. Burundi and the Bolivarian Republic of Venezuela have each implemented eight measures, while Zimbabwe has introduced seven.

Because these countries control significant shares of global supply, they possess greater market leverage and stronger incentives to manage exports strategically. The data suggests that motivations and policy approaches vary widely, ranging from security concerns and revenue generation to efforts to promote domestic processing.

These measures pursue different objectives, including raising government revenue, encouraging domestic value addition, and stabilizing cobalt prices amid a multi-year low in 2025.

The broader trend is clear: as demand rises and CETMs become increasingly strategic, governments controlling these resources are recognizing their leverage and integrating trade policy tools into broader economic strategies. Many are seeking to capture more domestic value by moving beyond raw material exports into processing and manufacturing, while also using export restrictions to advance national objectives.

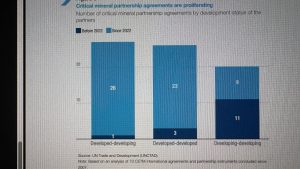

UNCTAD warned that the growing number of agreements, each with distinct rules, standards, and eligibility criteria, could create a “spaghetti bowl” of overlapping and sometimes inconsistent requirements. This could inadvertently increase transaction costs, complicate compliance, and create uncertainty for investors.

In some cases, divergent provisions could even impose competing or mutually exclusive conditions for participation in supply chains, undermining the efficiency and resilience these initiatives are intended to promote.

As competition for CETMs intensifies, critical-mineral-rich developing countries may face increasing pressure to align with one importing partner at the expense of others. Such choices could weaken the bargaining position of exporters and fragment global CETM trade into competing blocs, raising costs and reducing efficiency across the market.

Multilateral approach

UNCTAD said a more coordinated, multilateral approach could help avoid such an outcome. This would preserve developing countries’ ability to engage with multiple partners while ensuring that critical minerals trade remains open, competitive, and supportive of both the development needs of resource-rich countries and an affordable, timely global energy transition.